Bonvista Financial Services Pvt. Ltd.

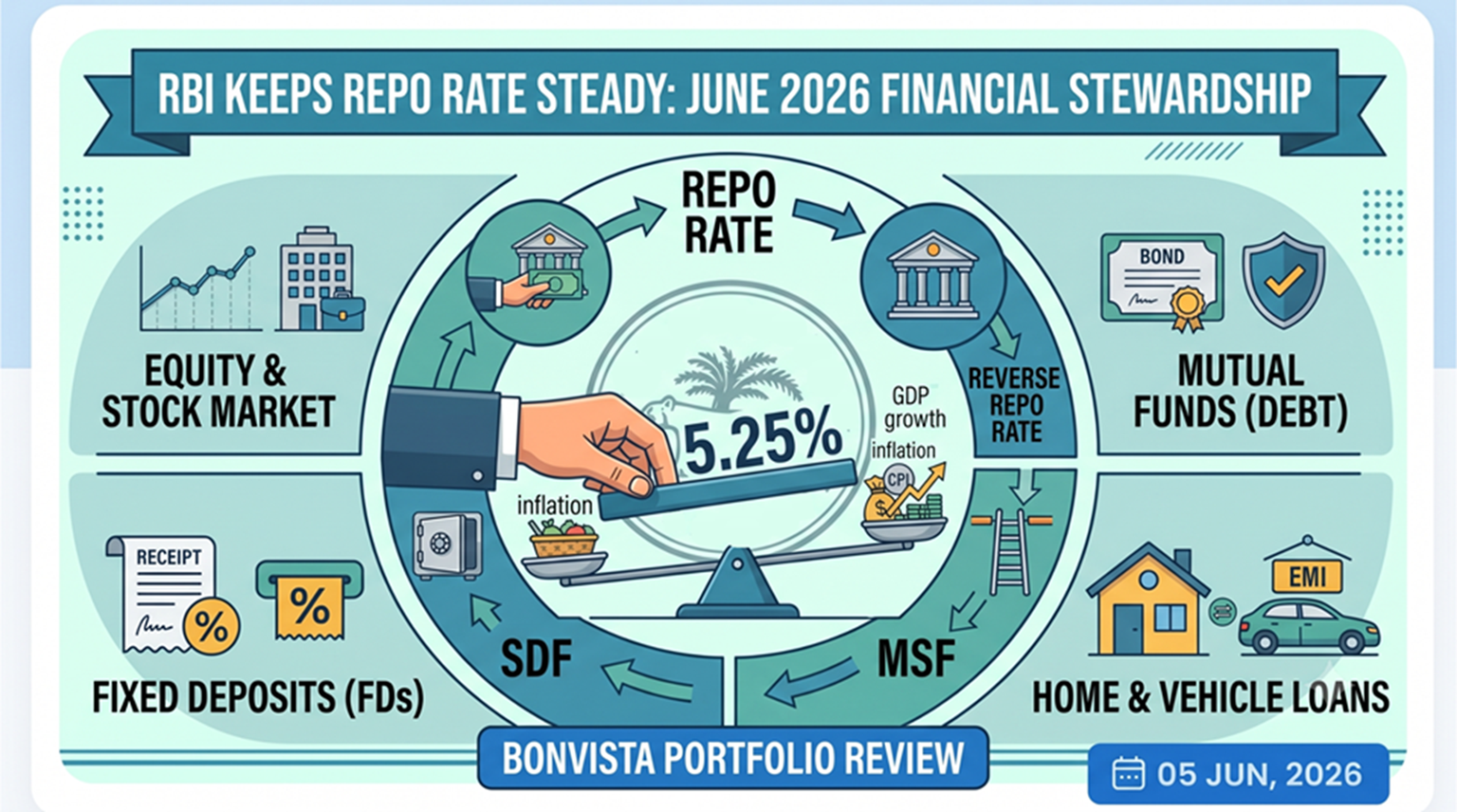

The world of investing runs on macroeconomics and policy benchmarks. For everyday retail investors, business owners, and salaried professionals, staying ahead of central bank updates is crucial for smart financial planning. The Reserve Bank of India (RBI), in its Monetary Policy Committee (MPC) meeting held on 5th June 2026, decided to keep the repo rate unchanged at 5.25% and maintained its "neutral" policy stance. This crucial decision reflects the central bank’s cautious approach as it carefully balances inflation concerns with domestic economic growth amid shifting global uncertainties.

For many people, RBI policy announcements often sound like technical financial jargon. Terms such as repo rate, reverse repo, SDF, and MSF may appear complicated. Still, these structural policy tools directly influence your personal borrowing costs, fixed deposit savings returns, mutual fund investments, and even short-term stock market movements.

Whether you are managing your family portfolio or seeking the best investment strategies, understanding these rates is the first step toward achieving true financial security. Let us break down exactly what these terms mean and how they affect retail investors on the ground.

What is the Monetary Policy Committee (MPC)?

The Monetary Policy Committee, commonly known as the MPC, is an elite six-member committee responsible for determining India’s benchmark interest rates and overall monetary policy framework. Its primary objective is to maintain price stability and curb inflation while safely supporting sustainable economic growth across the country.

The committee consists of:

-

The RBI Governor (serving as the Chairperson)

-

Two senior RBI officials

-

Three external macroeconomic experts appointed directly by the Government of India

The MPC usually meets every two months to evaluate the economic landscape and decide whether interest rates should be increased, decreased, or kept unchanged. These high-level decisions are largely influenced by retail inflation levels (CPI), domestic GDP growth metrics, global economic conditions, crude oil prices, and current financial market trends.

In this latest June 2026 review, the committee unanimously decided to maintain the repo rate at 5.25%, while firmly retaining a neutral stance. In banking terms, a neutral stance indicates that the RBI is neither signaling immediate rate hikes nor cuts. Instead, the central bank prefers to closely monitor incoming economic data and inflation patterns before taking future actions.

Join Our Financial Learning Community! Want to cut through the financial jargon and receive simplified daily market updates, economic insights, and wealth-building facts directly on your phone? Join our fast-growing WhatsApp community Paise ki Paathshala today: Join Kaise ki Paathshala Now

Understanding Key RBI Policy Rates

To properly manage your portfolio with a trusted wealth management service, you need to understand the four primary pillars of the RBI rate structure:

1. Repo Rate

The repo rate is the foundational interest rate at which the RBI lends short-term funds to commercial banks across India. Think of it as the base borrowing cost for the commercial banking system. If banks can borrow money cheaply from the central bank, they have the headroom to pass on lower lending rates to retail customers.

-

Current Repo Rate: 5.25%

-

Impact of a Rate Increase: Borrowing costs jump, home loan and vehicle loan EMIs rise, corporate expansion slows down, and consumer spending reduces to cool off inflation.

-

Impact of a Rate Decrease: Loans become significantly cheaper, monthly EMIs reduce, consumer consumption increases, and business investments get a strong growth boost.

2. Reverse Repo Rate

The reverse repo rate is the exact opposite: it is the interest rate at which the RBI borrows money from commercial banks. When commercial banks have surplus cash, they park those excess funds securely with the RBI to earn a guaranteed return. This tool helps the central bank manage and absorb excess liquidity from the active banking system. A higher reverse repo rate encourages banks to keep their cash safe with the RBI instead of lending it out aggressively to consumers.

3. Standing Deposit Facility (SDF)

The SDF is a modern monetary tool introduced to allow commercial banks to deposit unlimited excess liquidity with the RBI without requiring any government securities or collateral in return. The operational SDF rate is structurally linked directly to the primary policy rate: it is always set at Repo Rate minus 0.25%.

-

Current SDF Rate: 5.0%

-

Primary Purpose: Absorbing heavy excess liquidity from the financial ecosystem to maintain absolute macroeconomic stability.

4. Marginal Standing Facility (MSF)

The MSF acts as an emergency, last-resort borrowing window for scheduled commercial banks. If a bank faces a sudden, unexpected shortage of liquidity at the end of the day, it can borrow overnight funds from the RBI using its statutory liquidity ratio (SLR) portfolio. The emergency MSF rate is always pegged at Repo Rate plus 0.25%.

-

Current MSF Rate: 5.5%

-

Primary Purpose: Acting as a safety valve for the banking system. It costs more than standard repo borrowing because it is reserved strictly for urgent liquidity crunches.

What Does the Latest RBI Decision Mean for You?

By keeping these core interest rates unchanged and maintaining a neutral policy stance, the RBI is signaling a period of economic stability and predictability rather than aggressive marketplace intervention. Several key domestic and global factors influenced the MPC’s cautious decision:

-

Ongoing global geopolitical uncertainties and supply chain friction

-

Rising international crude oil prices are putting pressure on import bills

-

Persistent underlying food inflation risks

-

Currency-related stability concerns in the global forex market

-

The critical need to support domestic economic growth without triggering fresh inflationary pressures

The central bank is essentially taking a disciplined "wait and watch" approach to see how monsoon patterns and global financial cycles play out over the coming quarters.

Active Impact on Everyday Retail Investors

RBI policy updates influence your personal balance sheet far more than most people realize. Here is how this period of stability impacts your active asset allocation:

Equity and Stock Market Investors

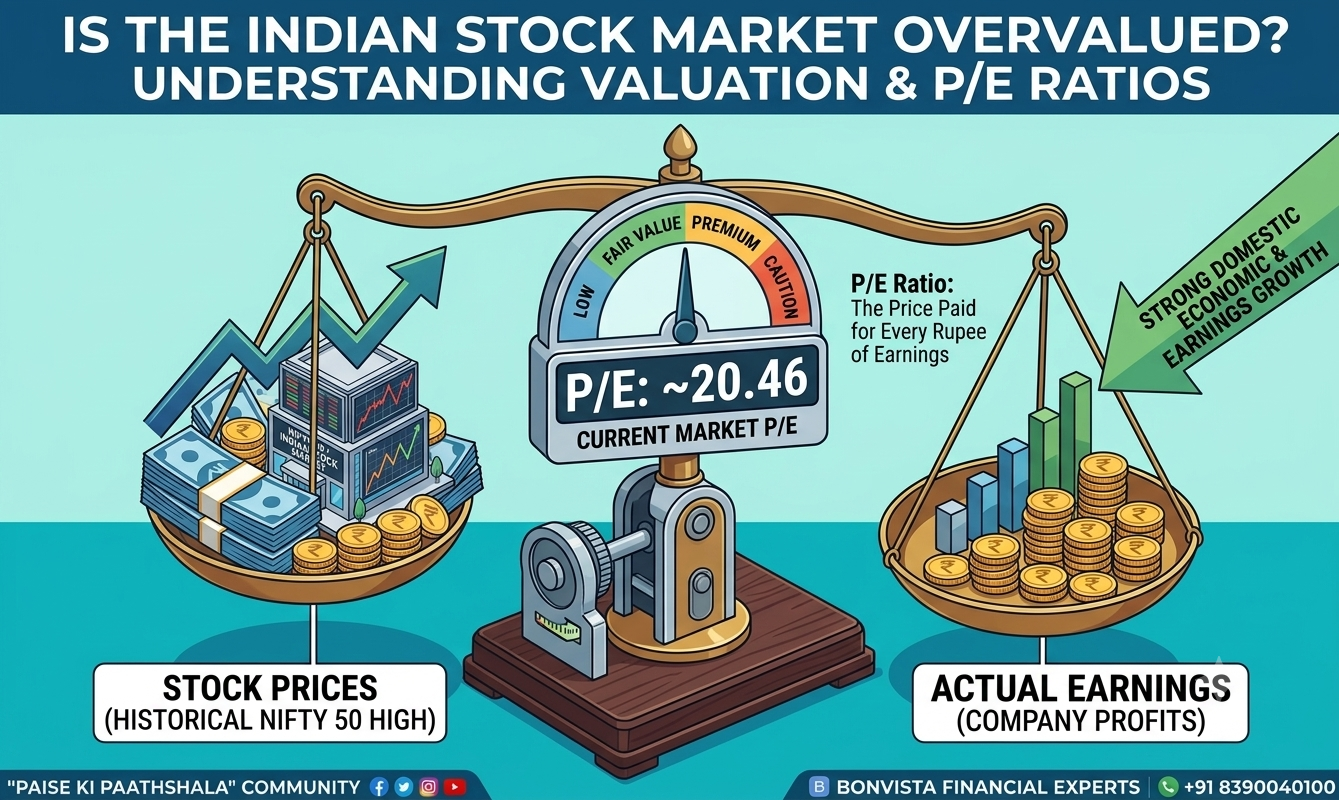

Stable interest rates generally provide a highly predictable operating environment for public corporations. Rate-sensitive sectors, such as banking, automobiles, real estate, and consumer finance, often react positively to stable, non-volatile borrowing costs. However, smart equity investors should continue focusing on long-term corporate business fundamentals and earnings visibility rather than making impulsive trades based solely on short-term policy updates.

Mutual Fund Investors

Debt mutual funds react directly to shifting interest rate trajectories. Since the RBI has chosen to keep policy rates on hold:

-

Short-duration and medium-duration debt mutual funds are positioned to deliver highly stable, predictable performance.

-

Overall bond market volatility is expected to remain well-contained in the near term.

-

Long-term debt funds will continue to track underlying retail inflation data closely to anticipate the next structural rate cut cycle.

Fixed Deposit (FD) Investors

For conservative investors relying on fixed-income products, the status quo means you should not expect major upward or downward shifts in fixed deposit rates immediately. Banks will likely maintain their existing interest rate slabs on retail deposits for the time being, making it a good window to lock in favorable yields before the eventual rate-cutting cycle begins.

Home and Vehicle Loan Borrowers

If you have an active home loan, a business loan, or a vehicle loan linked to an external benchmark lending rate (EBLR), you are unlikely to experience any major changes in your monthly EMI outgo in the short term. Your borrowing costs will remain steady, allowing for precise personal monthly budgeting.

Final Thoughts: Stability is an Opportunity

The RBI’s June 2026 monetary announcement might look like a simple "no-change" press release on the surface, but in complex financial environments, maintaining absolute policy stability is a powerful decision. By holding the repo rate steady at 5.25%, the central bank is successfully shielding the Indian financial ecosystem from external shocks while remaining laser-focused on keeping inflation under control.

For long-term retail investors, the takeaway message is simple: avoid making emotional adjustments to your portfolio based on short-term news headlines. The most effective way to build generational wealth is to keep a disciplined perspective, diversify across robust asset classes, and focus entirely on your specific life goals. Interest rate cycles will naturally come and go, but structural, goal-based financial planning remains your absolute strongest asset for long-term compounding.

Align Your Portfolio for the Remainder of 2026

Navigating macro updates, shifting interest rates, and multi-asset selection requires expert positioning. Let our certified advisory team help you optimize your mutual fund investments, evaluate high-alpha PMS options, and secure your long-term wealth milestones.

???? Take control of your financial journey. Click below to book an exclusive, personalized portfolio review with our expert financial planning team at Bonvista:

Request a Call from Our Wealth Experts at Bonvista

Follow for daily updates: WhatsApp | LinkedIn | YouTube | Instagram | Facebook | X | Pinterest

Disclaimer: This article is for educational and informational purposes only and does not constitute financial or investment advice. Investors should consult with their certified financial planner or wealth manager before making any investment decisions. Mutual fund and gold investments are subject to market risks.

Recent Posts

Gain control of

your life.

Contact Us

your life.