Bonvista Financial Services Pvt. Ltd.

Investors are aware that market fluctuations and securities volatility can affect mutual fund performance. However, returns on mutual funds are also influenced by the state of the national economy. Therefore, in a more general sense, changes in interest rates in India also lead to different returns from mutual funds. What is the precise relationship between interest rates and returns on mutual funds?

In this blog, let's learn everything there is to know.

What are Interest Rates?

The cost of borrowing money is known as the interest rate. It represents the starting point for all financial transactions. Interest rates are a crucial tool for managing economic activity in India, as they influence inflation, business investments, and consumer spending.

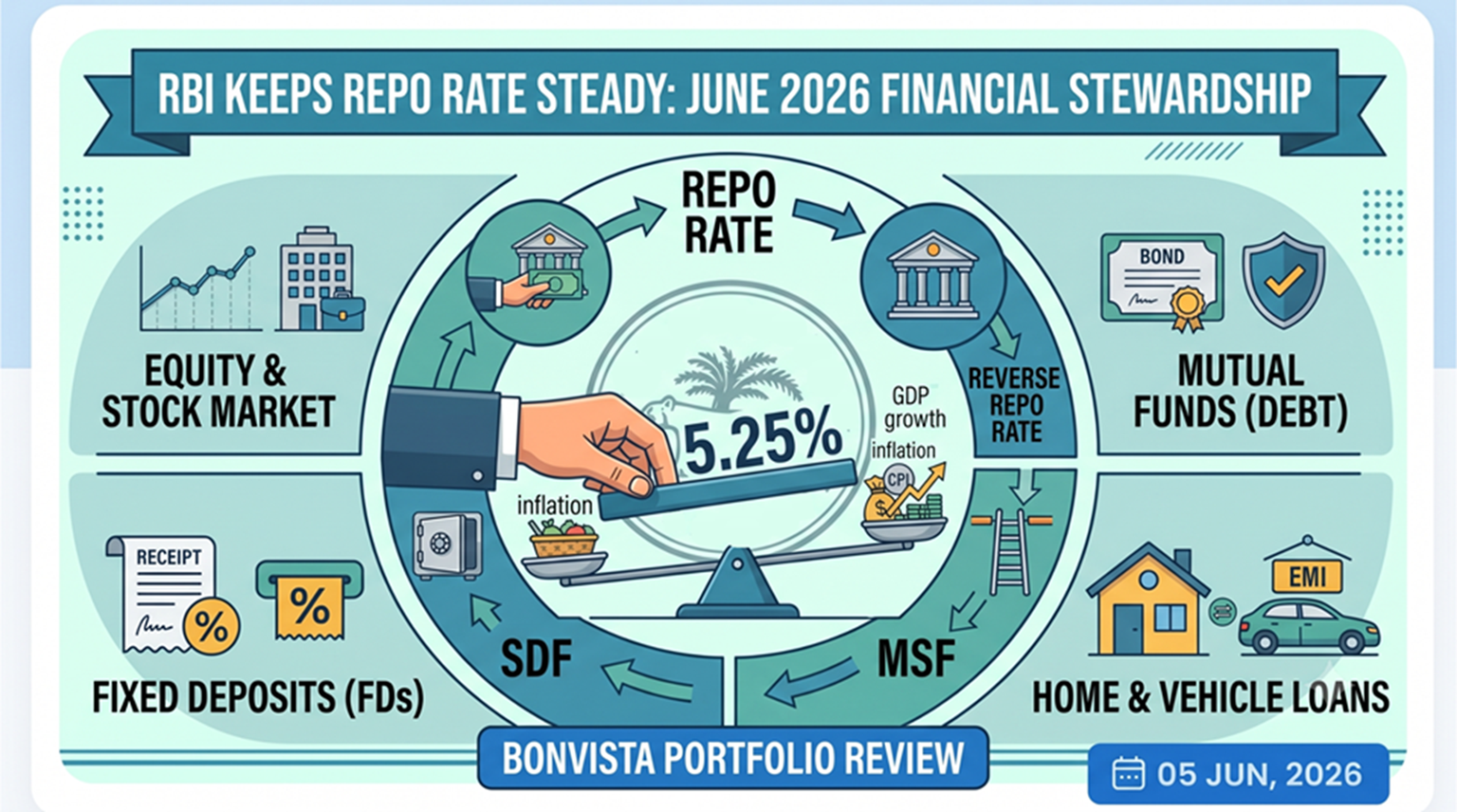

The RBI determines major interest rates, such as:

- Repo Rate: It is the rate at which banks borrow money from the RBI.

- Reverse Repo Rate: It is the rate at which the RBI borrows money from banks.

- Cash Reserve Ratio: The percentage of a bank's total deposits to be kept with the RBI. The purpose of CRR is to control the money supply in the country, manage inflation, and ensure the stability of the banking system.

These instruments assist the RBI in giving guidance for managing credit, inflation, and liquidity in the Indian economy.

What is the reason behind change in Interest Rates?

The economy of the world and the Indian economy are interconnected. Any increase in borrowing costs worldwide would be reflected in higher interest rates in India. Thus, the following factors influence interest rates:

-

- Inflation: In order to reduce excess demand in the economy, the RBI raises interest rates in response to high inflation. On the other hand, rate reductions are done to promote expenditure could result from low inflation.

-

- Fiscal Deficit: A significant fiscal deficit frequently results in increased borrowing by the government, raising interest rates.

-

- Global Market Trends: Indian interest rates are impacted by global economic factors, including changes in US Federal Reserve policy, particularly through international capital flows.

-

- Government Borrowings: As more money leaves the financial system, an increase in government borrowing pushes interest rates higher.

-

- RBI Monetary Policy Goals: The RBI's monetary policy seeks to strike a balance between inflation and growth. Interest rates are also impacted by the RBI's reviews of monetary policy.

Connection between Investment & Interest Rate

Interest rate changes have a variety of effects on investments due to shifting borrowing costs. The securities market will experience significant volatility during these periods. When interest rates fluctuate, investment choices and returns vary for the following reasons:

- Cost of Borrowing: A rise in interest rates raises the price of borrowing, including personal, auto, and house loans, which reduces disposable income. Interest rate reductions lower EMIs, boosting purchasing power.

- Savings Tools: Interest rate changes have a direct impact on fixed deposit rates as well as those of other saving plans like PPF, NSC & other traditional investment products.

- Market sentiment: Because fixed-income options are more alluring, high interest rates discourage stock market investments. And it is less expensive to raise capital, lower interest rates are seen as more equity-friendly.

How Interest Rates Impact Mutual Fund Investments?

Interest rates have an impact on mutual fund investments just like they do on any other type of investment. You need to understand how this operates in order to make wise financial choices.

Impact on Debt Mutual Funds:

Since debt mutual funds invest in fixed-income instruments like bonds and government securities, they are a particularly sensitive category to interest rate changes.

Bond prices decline when the RBI raises interest rates because newly issued bonds have higher yields than previously issued bonds, which makes the latter less appealing. On the other hand, bond prices increase when rates are dropped because there is a greater demand for existing bonds with higher yields.

When bond prices drop, debt fund NAVs typically do too. Compared to long-duration funds, short-duration funds are less affected. In the same manner, NAVs climb in line with bond prices, which greatly helps long-duration funds.

Impact on Equity Mutual Funds:

Changes in interest rates have an indirect impact on equities mutual funds by affecting market dynamics and corporate profitability. Companies' borrowing costs rise with higher interest rates, which lowers their profitability. Real estate and infrastructure, two industries that depend on debt finance, are particularly impacted. Reduced interest rates make borrowing less expensive and encourage company growth.

As lending rates rise, banks' margins may temporarily improve as well. During a rate hike, the infrastructure and real estate industries must pay higher borrowing costs, which is likely to impede growth. The FMCG and technology industries are less affected by rate fluctuations and typically draw investors during periods of high interest rates.

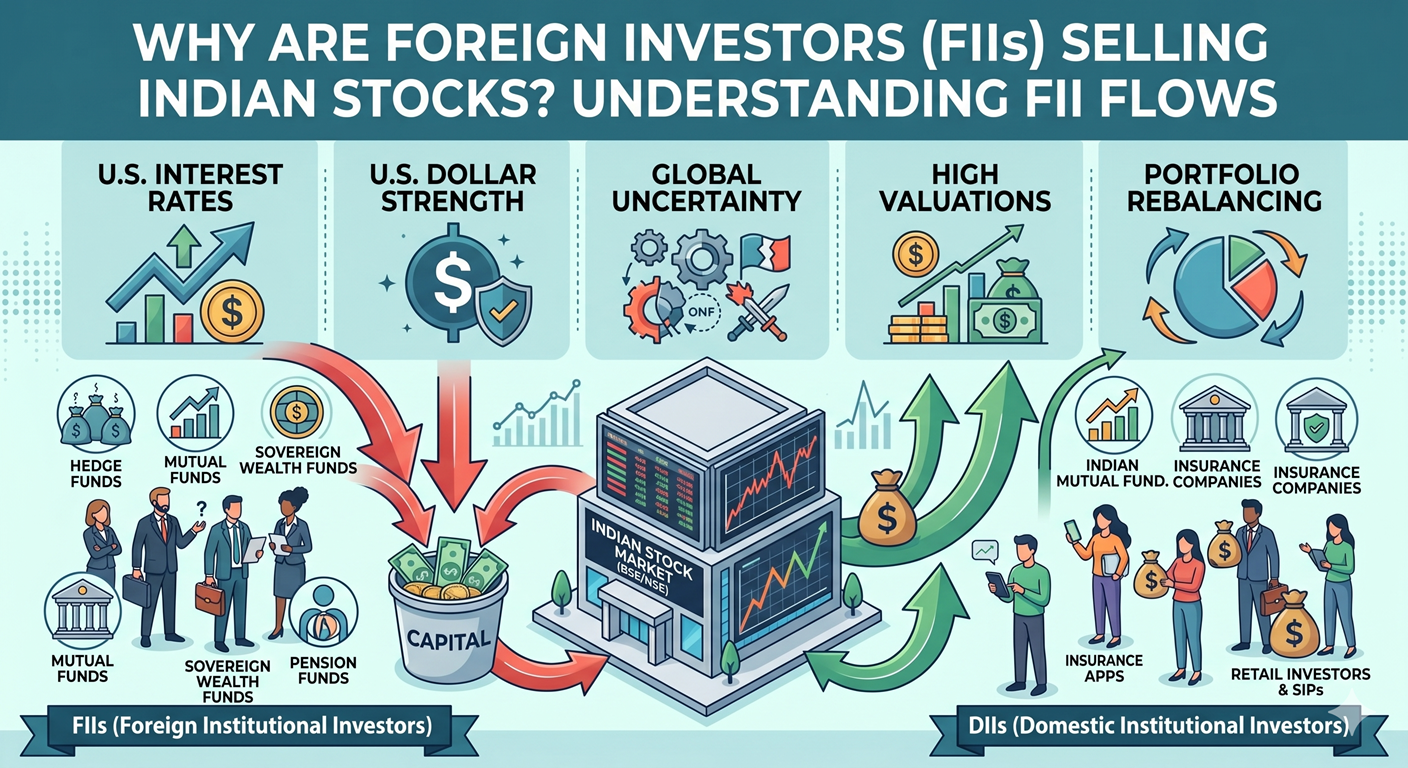

FIIs are typically drawn to the debt market by higher interest rates, which may cause stock market outflows. Conversely, lower interest rates encourage foreign investment in Indian stocks.

Impact on Hybrid Mutual Funds:

Hybrid mutual funds are sensitive to interest rate shocks since interest rates affect both debt and equity. To achieve the best possible risk-reward balance, a fund manager will reassemble the portfolio and oversee asset allocation. For example, exposure to the defensive equities and short-duration debt sectors will rise as interest rates rise.

What Can You Do to Protect Investments When Interest Rates Change?

With your wealth, threats cannot be eliminated. You can, however, adopt specific tactics to safeguard your investments when interest rates fluctuate. Here are some tactics that may be useful:

- During Rising Interest Rates: As the short-duration and ultra-short-duration debt funds invest in bonds with shorter maturities, they are less impacted by rate increases. When interest rates are rising, they provide stability and better returns than fixed deposits or savings accounts. When interest rates rise, it could be prudent to lessen exposure to the real estate and automotive industries.

- During Falling Interest Rates: As bond prices rise, long-duration debt funds profit from declining interest rates, which raises returns. You can think about boosting your investments in the FMCG and IT industries when interest rates decline.

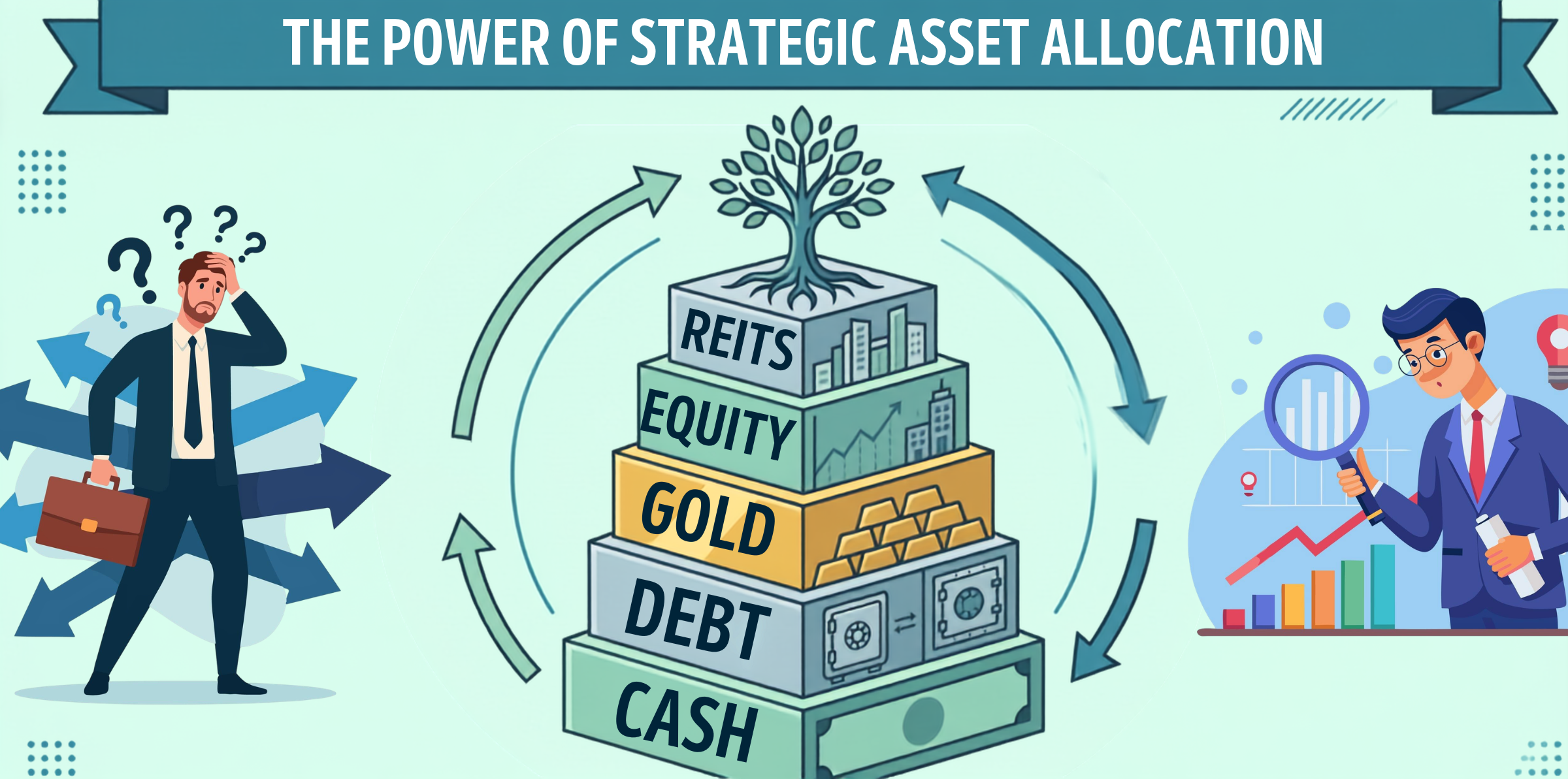

- Asset Allocation: To lower risk, spread your investments among debt and equity funds. Long-duration debt and growth-oriented stocks can profit from declining rates, while short-duration debt funds and defensive stocks can guard against increasing rates.

- SIPs and Hybrid Funds: While hybrid funds provide a balanced strategy by investing in both debt and equities and adjusting for fluctuating interest rates, SIPs aid in mitigating market volatility.

Conclusion:

All forms of investments and the return on investments are impacted by the RBI's changes to interest rates. Nonetheless, in both rising and declining interest rate scenarios, investors have the chance to optimize profits. To make sure that your investment strategy takes into account changes in investment rates, it is essential to conduct proactive and thorough portfolio monitoring. To reduce volatility and increase profits, always keep your portfolio diverse and incorporate SIP investments.