Bonvista Financial Services Pvt. Ltd.

When analysing investing, we frequently consider "returns"—the potential profit. However, correlation is another important concept that determines whether your portfolio increases steadily or causes you to have nightmares.

Let’s understand this in a very simple way.

What is the correlation?

Put, correlation refers to the movement of two investments in relation to one another.

- Two assets have a high correlation (almost +1) if they consistently move in the same direction.

- Their correlation is negative (around 1) if they travel in opposing directions.

- Correlation is low or close to zero if they move randomly and have no discernible relationship.

Why is Correlation Important in a Portfolio?

Consider investing your entire portfolio in a single stock, such as HDFC Bank Ltd. Your entire wealth is at risk if that stock fails. However, the risk of your entire portfolio is reduced if you include another company or asset that moves differently from HDFC Bank Ltd.

For this reason, investors advise against putting all of your eggs in one basket.

"Don't put all your money in assets that move together," is what they truly mean.

Let’s see some real-life examples:

- Nifty 50 vs Gold:

- Since gold is perceived as a secure asset, it typically appreciates during periods when the stock market declines, like as the COVID crash in March 2020. This indicates that there is little to no link between the Nifty 50 and gold. If your portfolio included both, your stock losses would have been offset by your gold profits.

- Nifty 50 vs Nifty IT

- Since they are both stocks, they often follow the same path. Both the Nifty 50 and the Nifty IT typically decline when the market declines. There is a substantial correlation here. Therefore, there is little risk reduction when IT stocks are added to a portfolio that is heavily weighted toward the Nifty.

- Equity vs Debt (Fixed Income Mutual Funds)

- Stock markets are volatile; they might rise or fall sharply. Generally speaking, debt (such as government bonds or debt mutual funds) yields consistent returns. The portfolio is more balanced because of its low correlation. As an instance, during the 2008 global financial crisis, Indian government bonds produced positive returns despite a steep decline in stocks.

Year 2008:

- Nifty 50: Fell by around -51%. The stock market crashed badly.

- Gold: Gave about +26% returns. People rushed to gold as a safe investment.

- Indian Govt Bonds: Gave around +10% returns. Safe and stable.

While stocks fell badly, gold and bonds protected investors.

Year 2017:

- Nifty 50: +28% (markets soared on growth optimism)

- Gold: Rose about 6% (mild positive return, much lower than equities)

- Bonds: ~+6–7% (stable as usual)

In good equity years, stocks outperform; gold and bonds act more like “shock absorbers” than wealth creators.

Year 2020:

- Nifty 50: Fell by around -23% during the COVID shock.

- Gold: Rose about +28% as investors again looked for safety.

- Bonds: Gave about +12%, stable returns.

Again, when stocks went down, gold and bonds went up.

Key Insight:

- Bad years for equities (2008, 2011, 2020): Gold shines, bonds steady.

- Good years for equities (2017, 2014, 2021): Nifty beats gold and bonds easily.

- Mixed/volatile years (2013, 2018): Bonds quietly deliver positive stability.

That’s the power of correlation: No single asset wins always, but the right mix of equity + gold + bonds makes the portfolio more stable.

Key Takeaways:

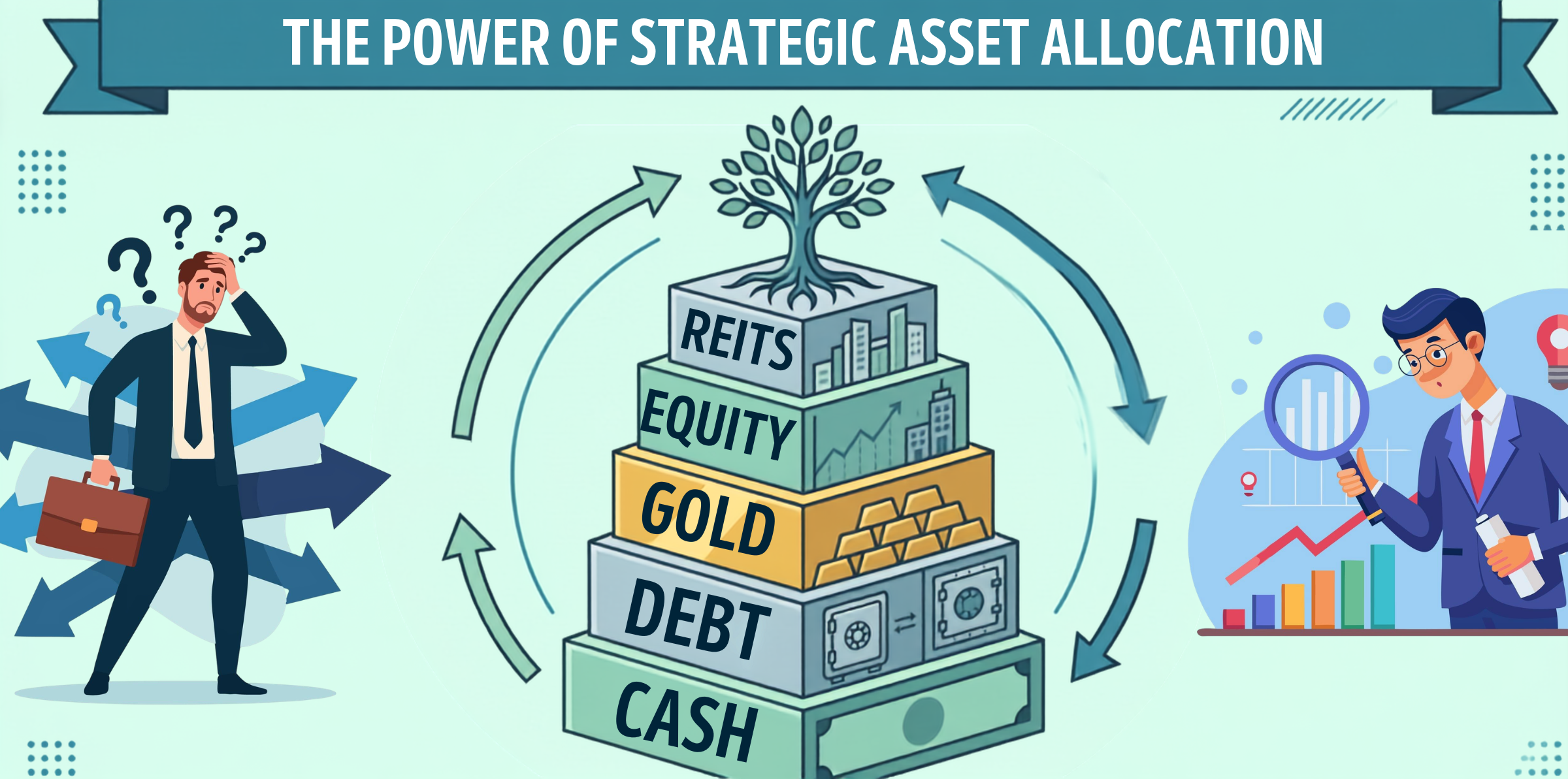

- Mixing different asset classes such as Equity, Debt, Gold, Real Estate, etc., with low correlation reduces overall portfolio risk. It will balance the portfolio returns.

- High correlation means higher risk.

- Smart diversification is not about the number of assets or the number of mutual fund schemes, but about different types of assets.

Chasing the higher returns isn't the only goal of investing. What matters is to create a portfolio that protects you in hard times and expands consistently. It is important to know how strongly or weakly your portfolio is correlated. By combining debt, equities, real estate, and gold, Indian investors can make the process of accumulating wealth easier.

Also Watch: Age 50 & Zero Savings? How to Build a ₹3 Crore Retirement Corpus | The Ultimate Plan

Gain control of

your life.

Contact Us

your life.